Bitcoin Tax Calculator

Transaction Details

Enter your Bitcoin purchase and sale details to calculate your capital gains or losses.

Calculation Results

Ever wondered why the IRS keeps asking about every Bitcoin move you make? The answer is simple: the tax code sees Bitcoin as property, not money. That means every time you buy, sell, trade, or even spend a single satoshi, there’s a taxable event to report. This guide breaks down what that property treatment looks like in practice, how you calculate gains or losses, and the most common pitfalls that can bite you at tax time.

Key Takeaways

- Bitcoin is classified as intangible property by the IRS, triggering gain/loss reporting on every transaction.

- Three tax categories exist - business property (mining), investment property (trading/holding), and personal property (personal purchases).

- Short‑term gains are taxed as ordinary income; long‑term gains qualify for 0%, 15% or 20% rates depending on your income.

- Hard forks and airdrops create ordinary‑income events when you receive new coins.

- Accurate record‑keeping (date, amount, fair market value, purpose) is essential - most taxpayers rely on crypto‑tax software.

Why the IRS Calls Bitcoin Property

Bitcoin is a digital asset that the Internal Revenue Service (IRS) classifies as intangible property. The ruling came in Notice 2014‑21, released in March 2014, and it has held steady through 2025. The agency treats Bitcoin like any other piece of property - think of a painting or a piece of real estate. Whenever you exchange it, the IRS expects you to calculate a gain or loss based on the difference between your basis (what you paid) and the fair market value at the time of the transaction.

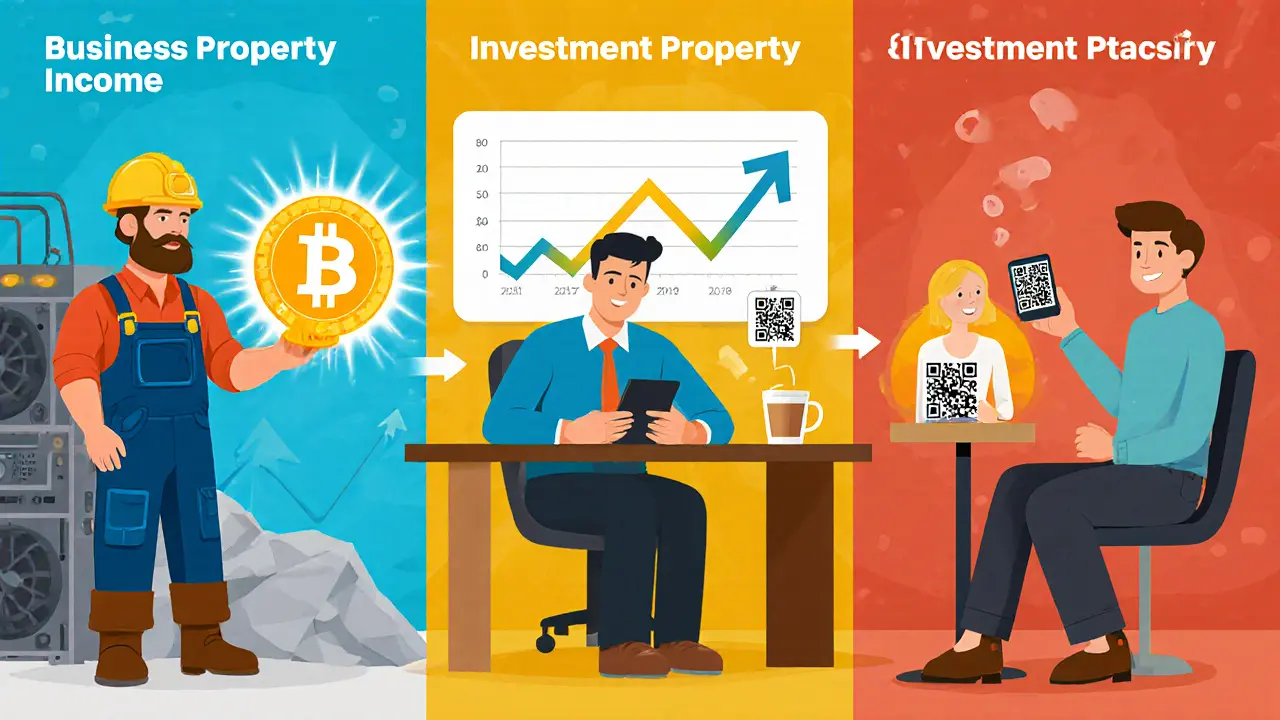

The Three Property Classifications

Depending on how you acquire and use Bitcoin, the tax treatment can differ dramatically.

- Business property: If you mine Bitcoin as part of a trade or business, the fair market value of the mined coins is ordinary income on the day you receive them. Subsequent sales are taxed as capital gains.

- Investment property: Most owners fall here - you buy Bitcoin hoping it will go up. If you hold it for more than a year before selling, any profit is a long‑term capital gain; otherwise, it’s short‑term.

- Personal property: When you use Bitcoin to buy a coffee or a laptop, the transaction still triggers a taxable event. The gain or loss is calculated just like an investment sale.

Calculating Basis and Gain

For every transaction, you need three data points: purchase date, purchase price (your basis), and the fair market value at disposal. The IRS permits two accounting methods for allocating basis when you sell only part of your holdings:

- Specific identification: You pick which Bitcoin lots you’re selling. This works only if you have detailed records for each purchase.

- First‑in‑first‑out (FIFO): In the absence of specific identification, the oldest coins are considered sold first.

Let’s walk through a quick example from the guidance:

- April 15: bought 1.0BTC for $20,000

- June 15: bought 0.5BTC for $18,000

- December 10: sold 1.5BTC for $32,000

Your total basis is $38,000. Using FIFO, the first 1.0BTC (basis $20,000) is sold first, followed by 0.5BTC (basis $18,000). The $32,000 proceeds create a loss of $6,000, which you can deduct against other capital gains.

Capital Gains Rates in 2024‑25

| Filing Status | 0% Rate Threshold | 15% Rate Range | 20% Rate Above | Short‑Term (Ordinary) Rate Max |

|---|---|---|---|---|

| Single | $47,025 | $47,026 - $518,900 | >$518,901 | 37% |

| Married Filing Jointly | $94,050 | $94,051 - $583,750 | >$583,751 | 37% |

| Head of Household | $63,000 | $63,001 - $551,350 | >$551,351 | 37% |

Keep in mind that the thresholds adjust each year for inflation, so always check the latest IRS tables before filing.

Hard Forks, Airdrops, and the Tax Implications

When a blockchain splits, the tax treatment depends on whether you receive a new coin automatically or through an airdrop.

- Hard fork without new coins: No taxable event if you don’t receive any additional tokens.

- Hard fork with airdrop: The moment you gain control over the new coins (recorded on the ledger, you can transfer or sell them) you must recognize ordinary income equal to the fair market value at that moment. The basis of the airdropped coins equals that income amount.

These rules come from the IRS’s 2019 revenue ruling, which clarified that receipt occurs when you have “dominion and control” over the cryptocurrency.

Legislative Landscape: GENIUS Act and CLARITY Bill

Both the GENIUS Act (signed July2025) and the pending CLARITY Bill aim to modernize crypto regulation but they haven’t altered the fundamental IRS stance. The agency still treats crypto as property unless a specific provision of the Internal Revenue Code says otherwise. That means even if the SEC labels a token a security, the tax treatment remains unchanged.

Practical Tips for Staying Compliant

Here’s a short checklist you can follow throughout the year:

- Record every Bitcoin transaction - date, amount, USD value, purpose, and counterparties.

- Choose an accounting method (specific ID or FIFO) and stick with it.

- Use reputable crypto‑tax software to import exchange data and generate Form 8949 entries.

- Watch for hard forks and airdrops - note the fair market value on the day you gain control.

- Report crypto holdings on the 2020‑2025 Form 1040 question: “Did you receive, sell, send, or otherwise acquire any virtual currency?”

- If you mine Bitcoin, report the fair market value as ordinary income on Schedule C.

Missing a single transaction can trigger an audit. The IRS has been ramping up enforcement, especially for high‑volume traders.

Common Pitfalls and How to Avoid Them

- Mixing personal and business use: Keep separate wallets if you both mine and invest.

- Assuming crypto‑to‑crypto swaps are tax‑free: Each swap is a taxable disposition of the first coin and acquisition of the second.

- Relying on exchange PDFs alone: Some platforms don’t report fees or partial fills accurately; double‑check against your own logs.

- Forgetting the cost basis of airdropped coins: The IRS expects you to treat the FMV at receipt as both income and basis.

Bottom Line for Bitcoin tax Planning

Treating Bitcoin as property makes the tax landscape dense, but it also gives you tools to manage liability. By tracking every move, choosing the right accounting method, and staying aware of legislative updates, you can avoid nasty surprises when April rolls around.

Frequently Asked Questions

Do I have to report every tiny Bitcoin purchase?

Yes. The IRS expects a record for each acquisition, no matter how small. If the total amount of all purchases is under $10,000 you still need to report gains or losses when you dispose of the coins.

How do I calculate basis for Bitcoin received as payment for services?

The fair market value in US dollars on the day you receive the Bitcoin counts as ordinary income and also becomes your cost basis for future sales.

Can I use the like‑kind exchange rules for Bitcoin?

No. The Tax Cuts and Jobs Act of 2017 limited like‑kind exchanges to real property. Bitcoin swaps are always taxable events.

What happens if I forget to report a hard‑fork airdrop?

The IRS can assess penalties for under‑reporting income. If you discover the omission later, file an amended return (Form 1040‑X) with the missing income and pay any interest.

Do I need a CPA if I trade Bitcoin frequently?

While not required by law, a CPA familiar with crypto can help you navigate complex transactions, especially if you have hundreds of trades. They can also ensure your Form 8949 is accurate and help you claim any available deductions.

Dimitri Breiner

October 10, 2025 AT 06:02Just wanted to say this guide is one of the clearest I’ve seen on crypto taxation. The breakdown of business vs. investment vs. personal property is exactly what people need to stop guessing. I’ve helped three friends file their crypto taxes this year using this as a reference - no audits, no panic, just clean reporting.

Ashley Cecil

October 10, 2025 AT 14:58It is imperative to note that the IRS’s classification of Bitcoin as property is not a suggestion-it is a legal mandate under Section 1001 of the Internal Revenue Code. Failure to report even the smallest transaction constitutes tax evasion, and the penalties are neither trivial nor discretionary.

Joseph Eckelkamp

October 11, 2025 AT 03:00So… we’re still pretending that buying a $5 coffee with Bitcoin is equivalent to selling a stock? Brilliant. We’ve got a tax code designed for 19th-century land deeds trying to track digital tokens that move at the speed of light. And yet, somehow, the IRS expects us to track every satoshi like it’s a vintage wine collection? I’ll take my $6,000 loss and my existential dread, thanks.

LeAnn Dolly-Powell

October 11, 2025 AT 18:05This is so helpful!! I was so stressed about my airdrops last year, but now I know exactly what to report. You’re not alone-so many people are scared to even look at their crypto tax forms. You’re doing great ❤️

Anastasia Alamanou

October 12, 2025 AT 12:34From a compliance standpoint, the FIFO methodology, while administratively convenient, introduces significant distortions in basis allocation-particularly in volatile markets where the temporal dispersion of acquisition events creates non-representative cost bases. I recommend, where feasible, leveraging specific identification protocols to mitigate potential overstatement of short-term capital gains.

adam pop

October 12, 2025 AT 18:10They call it property? Ha. The IRS knows crypto is a decentralized network they can’t control. This is all just a trap. They’re building a ledger to track every wallet, every transaction, so they can freeze your assets later. They’ve been doing this since the 80s with gold. Don’t fall for it.

Jennifer Rosada

October 13, 2025 AT 12:02It’s not just about compliance-it’s about integrity. If you’re using Bitcoin to avoid reporting income, you’re not being clever, you’re being dishonest. And yes, that includes those ‘small’ transactions. You think the IRS doesn’t cross-reference exchange data with bank deposits? Please. You’re not a hacker-you’re just a taxpayer who forgot to do their homework.

John E Owren

October 14, 2025 AT 03:20For anyone overwhelmed by the rules: start simple. Pick one accounting method, use a trusted tool like Koinly or CoinTracker, and just get your records organized. You don’t need to be an expert-you just need to be consistent. Progress over perfection.

Gabrielle Loeser

October 14, 2025 AT 13:56I appreciate how this guide acknowledges that people aren’t just speculators-we’re users. Buying coffee with BTC, sending money to family abroad, even mining on a small scale: these aren’t loopholes, they’re real-life financial behaviors. The tax system needs to evolve to meet people where they are, not punish them for using new tools.

Rohit Sreenath

October 14, 2025 AT 14:11Bitcoin is not money. Money is printed by governments. This is just digital magic. You pay tax on magic? That is stupid.